Follow

Linkedin

Now

Week

Month

How Charlie Ledley and Jamie Mai turned $110,000 into almost $130 million

How to develop, test and optimize a trading strategy – complete guide

Ed Thorp’s Remarkable Journey: From Beating Casinos to Dominating Wall Street

Brainstorming Ideas To Create Winning Crude Oil Trading Strategy

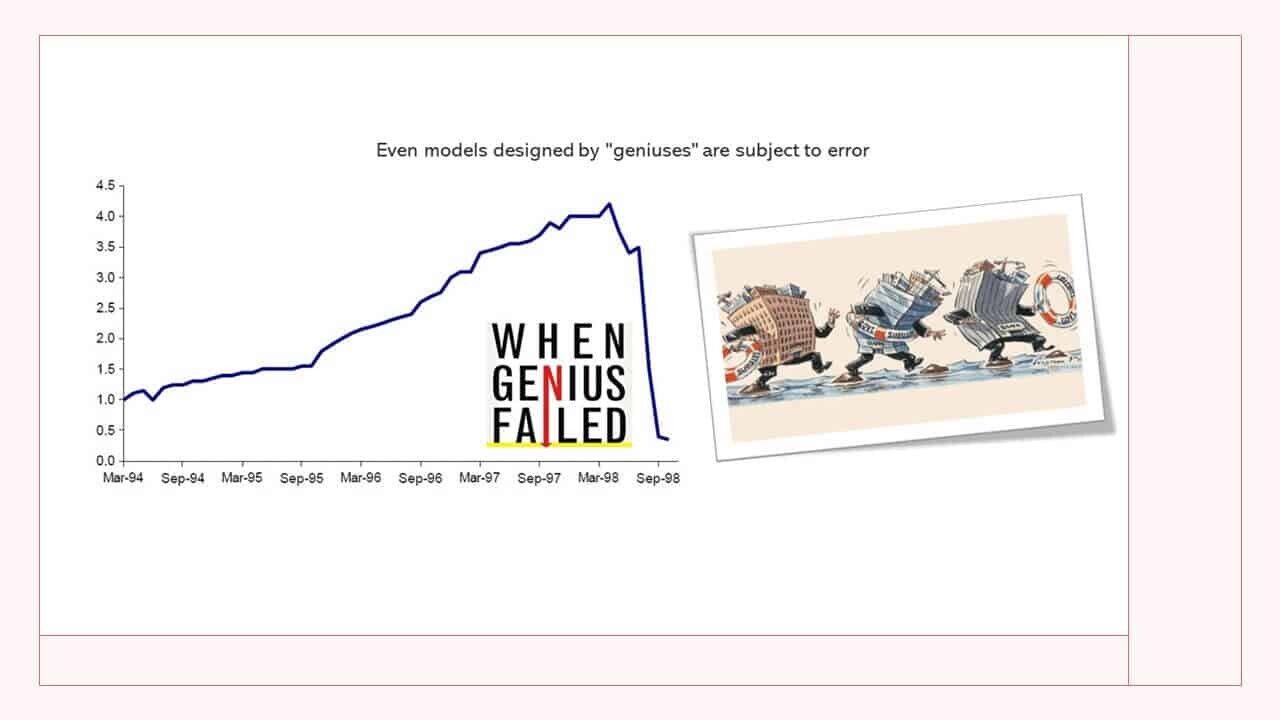

What We Can Learn From The Long Term Capital Management Hedge Fund Collapse

Wealth Hub

Trading Magazine

Free Articles

Resources

Hedge Fund Letters

List of Libraries for Quants

Recommended Reading

Machine Learning Courses

Research Papers

Financial Glossary

Contact Us

About Us

About Us

Investment Mandates

Write for Us

Terms of Service

Client Portal

Login Account

Trading Strategies

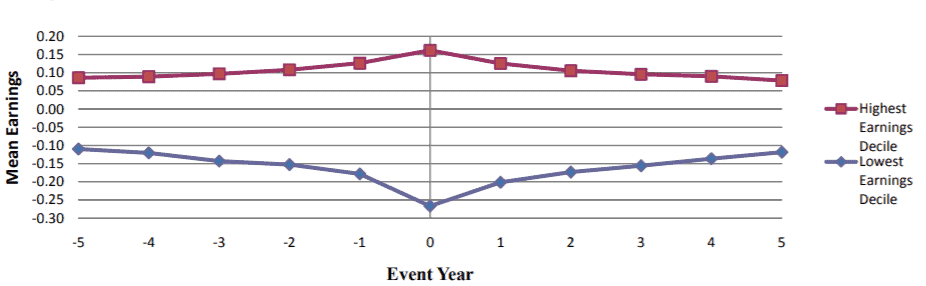

Identifying Anomalies in Capital Markets: Accrual Anomaly

How to develop, test and optimize a trading strategy – complete guide

Mastering Mean Reversion Trading: A Guide to Identifying and Capitalizing on Range Bound Formations

Build a Trading System using Statistical Methods

How Charlie Ledley and Jamie Mai turned $110,000 into almost $130 million

Demystifying Bollinger Bands

Mean Reversion Volatility Strategy

Mean Reversion Trading System

Spot Price Patterns with the COT Report

Trading with different time frames

Posts pagination

1

2

3

4

Scroll To Top

Wealth Hub

Trading Magazine

Free Articles

Resources

Hedge Fund Letters

List of Libraries for Quants

Recommended Reading

Machine Learning Courses

Research Papers

Financial Glossary

Contact Us

About Us

About Us

Investment Mandates

Write for Us

Terms of Service

Client Portal

Login Account

Linkedin