Follow

Linkedin

Now

Week

Month

How to develop, test and optimize a trading strategy – complete guide

How Charlie Ledley and Jamie Mai turned $110,000 into almost $130 million

The Complete Guide to Portfolio Optimization in R PART1

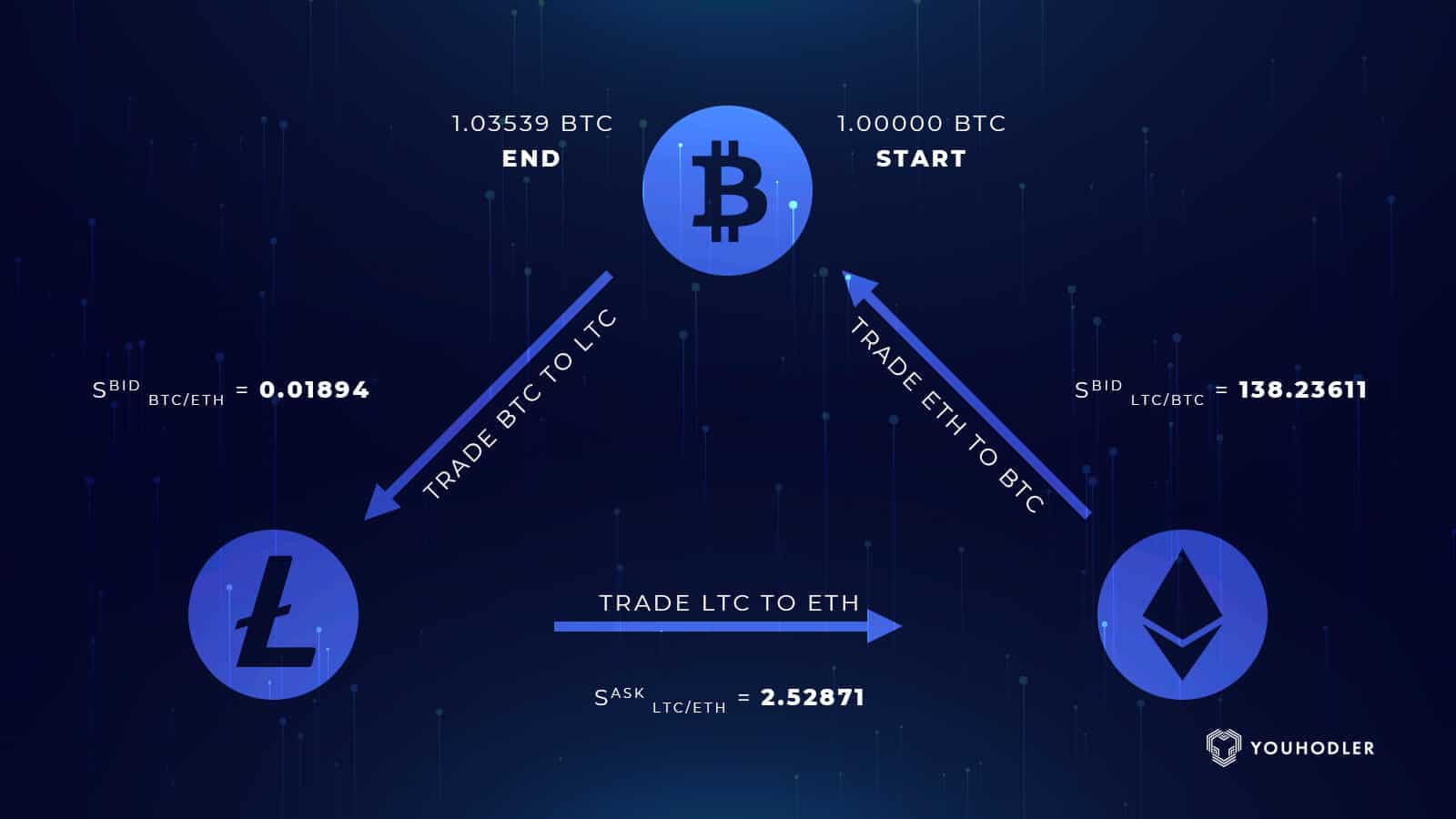

Unveiling the Secrets of Profitable Cryptocurrency Arbitrage: A Comprehensive Guide

Pairs Trading – A Real-World Profitable Strategy

Wealth Hub

Trading Magazine

Free Articles

Resources

Hedge Fund Letters

List of Libraries for Quants

Recommended Reading

Machine Learning Courses

Research Papers

Financial Glossary

Contact Us

About Us

About Us

Investment Mandates

Write for Us

Terms of Service

Client Portal

Login Account

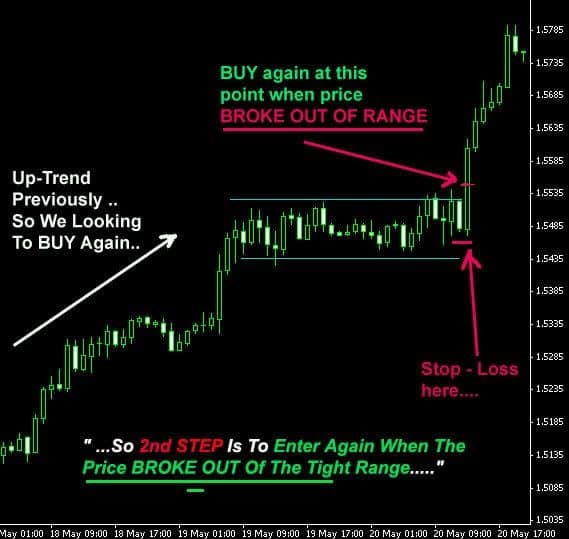

Mean Reversion Volatility Strategy

Mean Reversion Trading System

Spot Price Patterns with the COT Report

Video Wall Street Code

Trading with different time frames

10 Key Points in a Companies 10Q Report

Applied Statistics for Futures Markets

The Fine Art of Opening Range Breakout Trading and How to Master It

Supercharge Seasonal Movement Analysis

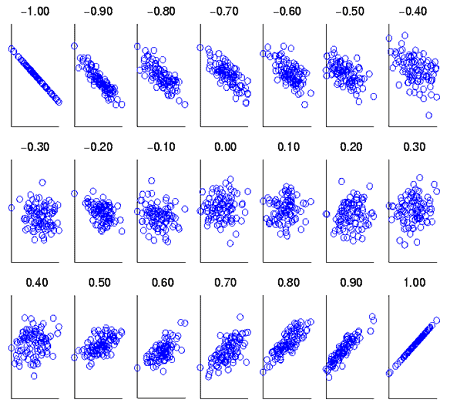

Optimum Asset Allocation using Correlation

Posts pagination

1

2

3

Follow @Milton_FMR

Categories

Fundamental Analysis

Hedge Fund Analysis

Market News

Quantitative Analysis

Risk Management

System Development

Trading Strategies

Videos

miltonfmr.com

Unlock the Secrets of Seasonal Trading: Proven Strategies and Real Data to Boost Your Returns

The Illusion of Endless Prosperity: Unraveling the Crash of 1929 and its Prolonged Aftermath

Ed Thorp’s Remarkable Journey: From Beating Casinos to Dominating Wall Street

The Institute Reads

Turing Finance

Quantocracy

Project Syndicate

Yanis Varoufakis

Wolf Street

The Economist

Zerohedge

Scroll To Top

Wealth Hub

Trading Magazine

Free Articles

Resources

Hedge Fund Letters

List of Libraries for Quants

Recommended Reading

Machine Learning Courses

Research Papers

Financial Glossary

Contact Us

About Us

About Us

Investment Mandates

Write for Us

Terms of Service

Client Portal

Login Account

Linkedin