Follow

Linkedin

Now

Week

Month

How Charlie Ledley and Jamie Mai turned $110,000 into almost $130 million

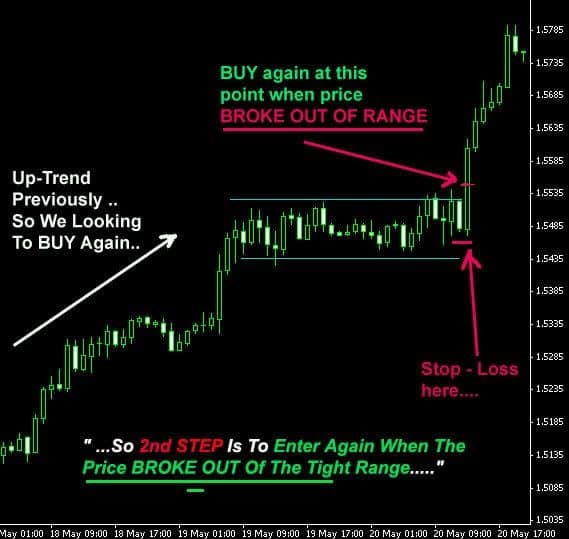

The Fine Art of Opening Range Breakout Trading and How to Master It

How to develop, test and optimize a trading strategy – complete guide

Ed Thorp’s Remarkable Journey: From Beating Casinos to Dominating Wall Street

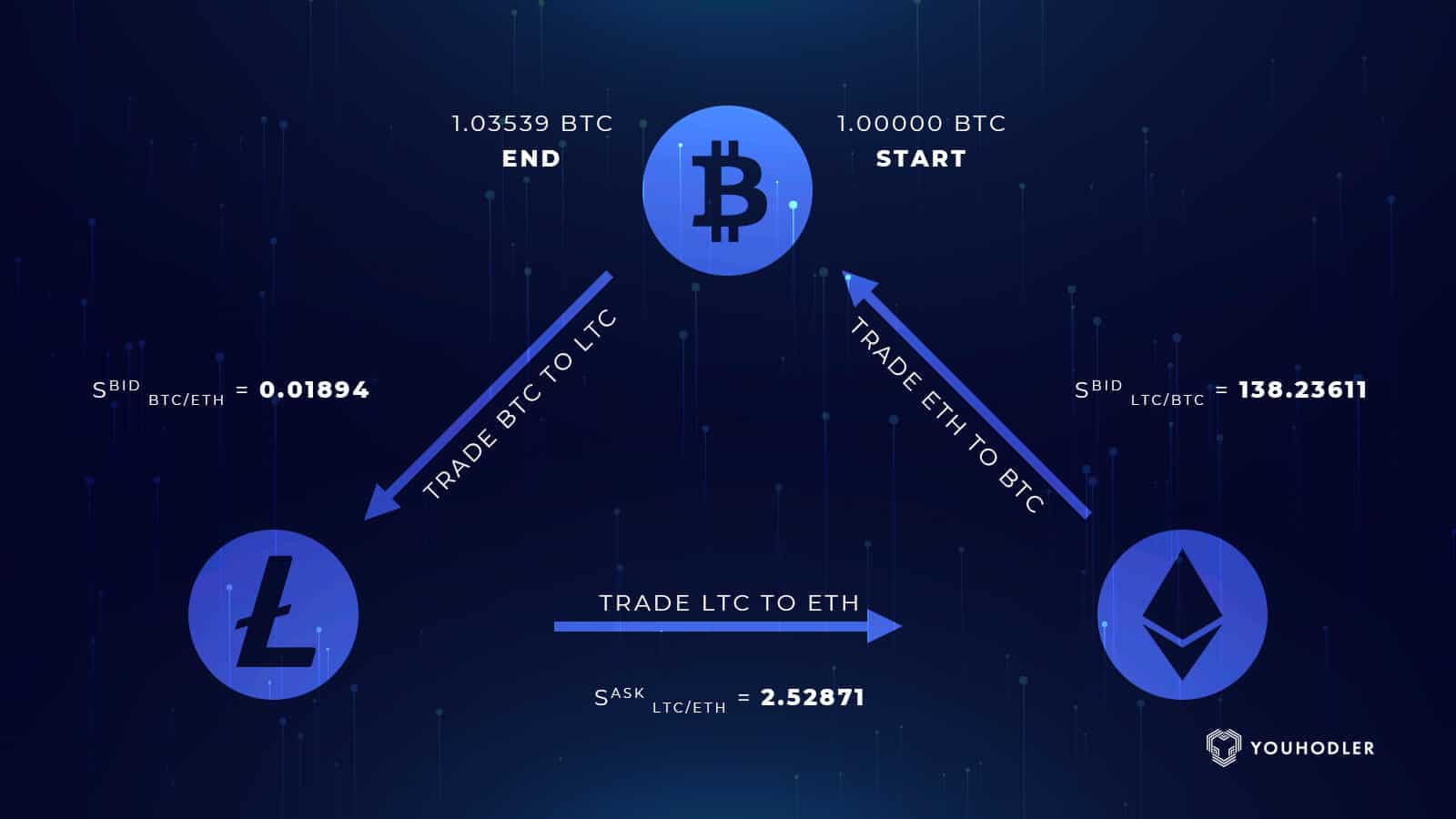

Unveiling the Secrets of Profitable Cryptocurrency Arbitrage: A Comprehensive Guide

Wealth Hub

Trading Magazine

Free Articles

Resources

Hedge Fund Letters

List of Libraries for Quants

Recommended Reading

Machine Learning Courses

Research Papers

Financial Glossary

Contact Us

About Us

About Us

Investment Mandates

Write for Us

Terms of Service

Client Portal

Login Account

Analysis

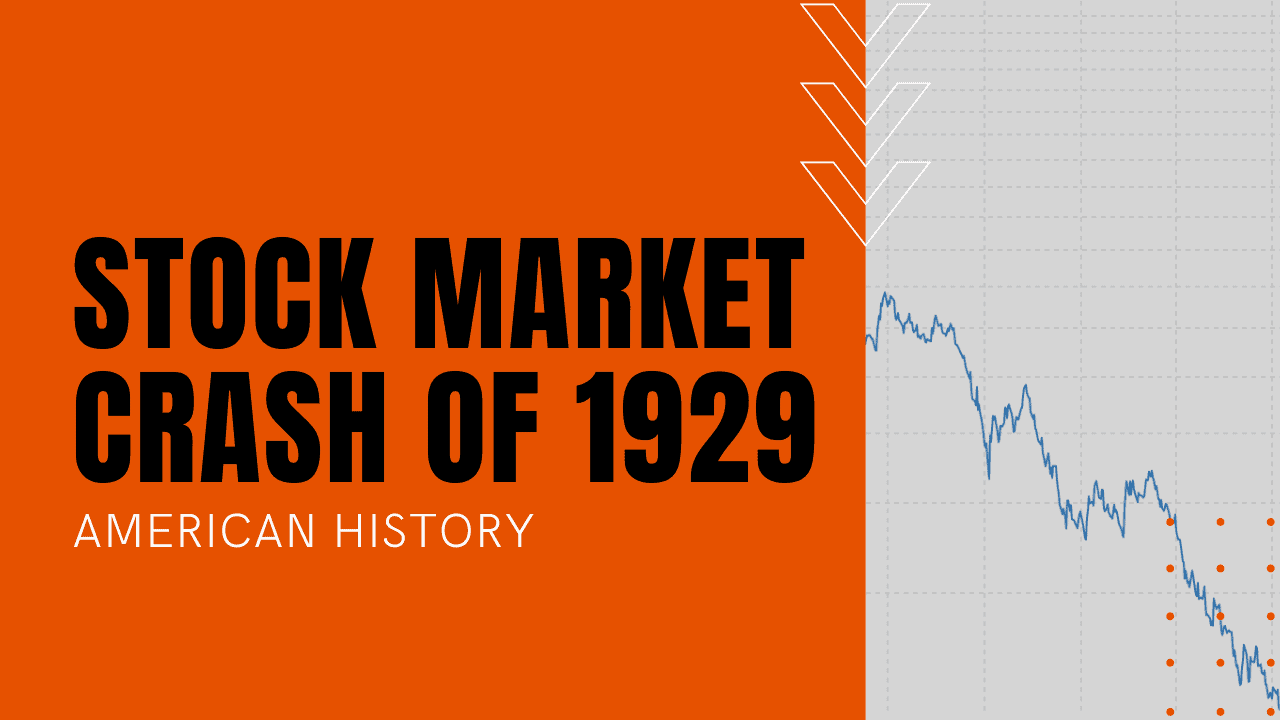

The Illusion of Endless Prosperity: Unraveling the Crash of 1929 and its Prolonged Aftermath

Unlocking the Power of Emotions: Deciphering the Fear & Greed Index

SEC Filings Analytics: Forms You Need To Know For Hot Stock Picks

Securities Class Action Filings February

Trading with different time frames

Applied Statistics for Futures Markets

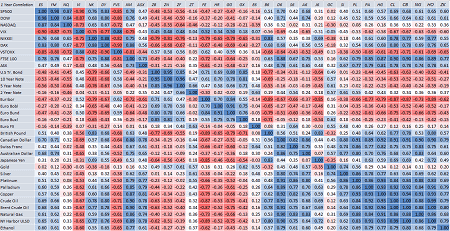

Inter-Market Correlations

Volume Trading Strategy

Analyzing Economic Indicators

Most Important Economic Indicators

Posts pagination

1

2

Scroll To Top

Wealth Hub

Trading Magazine

Free Articles

Resources

Hedge Fund Letters

List of Libraries for Quants

Recommended Reading

Machine Learning Courses

Research Papers

Financial Glossary

Contact Us

About Us

About Us

Investment Mandates

Write for Us

Terms of Service

Client Portal

Login Account

Linkedin